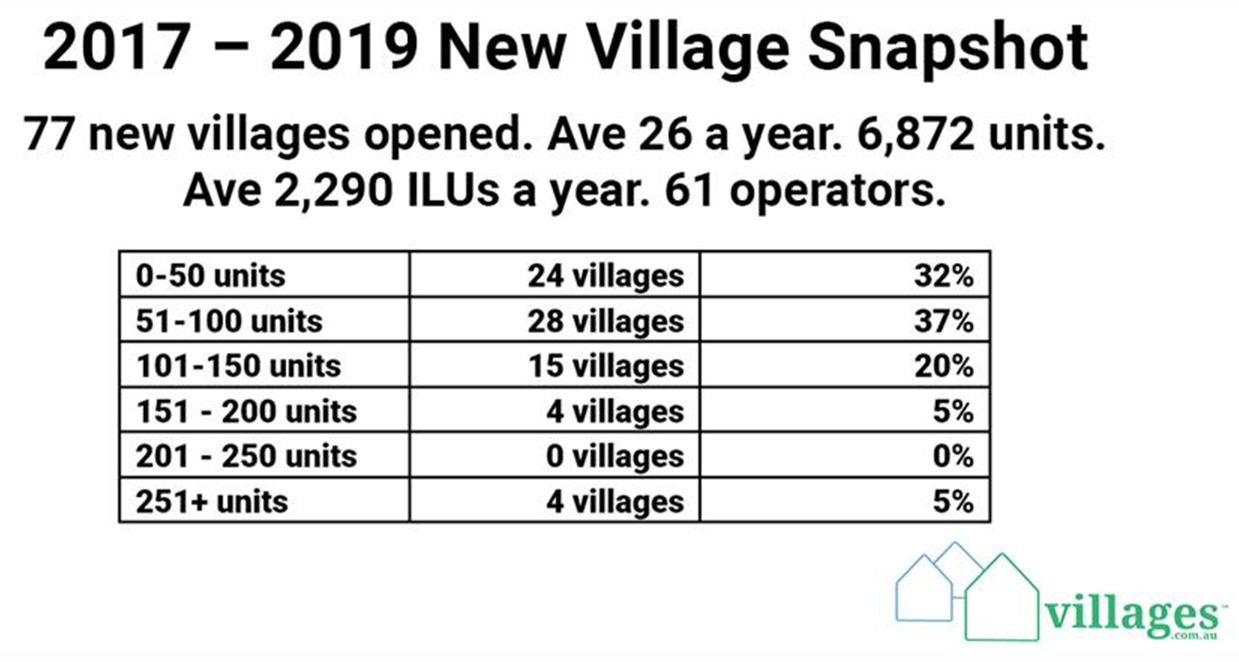

Last week I was asking if the retirement village sector had lost its mojo, with just 2,290 new village homes being built and delivered each year since 2017 by an average of 27 operators each year (out of 800 operators in the sector).

This means that village ‘penetration’ is going backwards, as we need to develop 5,500 new homes a year to maintained the historic 6% of all people aged 65+ living in villages.

Planned new village growth up 50%

This week we get the news that NZ’s Ryman has revised its forecasts and will be adding 800 new homes in Victoria every year (and expanding into other states) for the foreseeable future, plus Oak Tree is murmuring it will increase its activity.

This week we get the news that NZ’s Ryman has revised its forecasts and will be adding 800 new homes in Victoria every year (and expanding into other states) for the foreseeable future, plus Oak Tree is murmuring it will increase its activity.

NZ’s Summerset is also well advanced with land for two villages, also in Melbourne. Between the three they could increase the number of village homes being built by 50% a year.

AOR/DCM Research says 3% could be 18%

At the same time, our DCM Research unit has completed its Prospect Profile research, conducted by AOR, which identifies that while just 3% of the 65+ population are actively considering retirement villages, the village path is open to 18% of the population.

Monica Gessler of AOR opens her report:

“The sector is at a critical juncture where there exists enormous opportunity for growth. This is not just about maintaining sales, but creating a shift change in our society in the need the sector fulfills.”

“The Australian population is ageing. At the same time, COVID-19 has exposed the vulnerabilities of the oldest members of society.”

“In a culture where independence and control over one’s life is paramount, the importance of maintaining this sense of independence and control as one ages has grown. The compelling role of retirement villages is to enable this.”

3% represents 74,100 customers. 18% represents 441,600 customers.

3% represents 74,100 customers. 18% represents 441,600 customers.

The research identifies the obstacles, but also the growth path to sales at an individual village level. 5,500 new unit sales a year is highly achievable.

Land lease at 2,100 new units now

Then we obtained the Ingenia Citi Conference presentation from last week, with the chart at the top.

It identifies that land lease community penetration is 2.1%, which is what you would expect from a young sector. They identify that 1,500 to 2,000 new LLC homes are being built a year, about the same as retirement villages, and by 2026 this will increase to 2,700 if they maintain the 2.1% penetration.

If this is the case, retirement villages will leave LLCs in the dust in new developments.

LLC sector finding its feet

There is no doubt about the appealing metrics of the land lease business model – aspirational lifestyle appeal, affordable housing, firm sale, fast build and the biggest market segment.

But the sector is still young, with the limited number of large players are managing growth, and an increasing number of small players are learning about managing a resident population for the first time.

But the biggest LLC constraint is the development cycle, which is a three- to five-year journey.

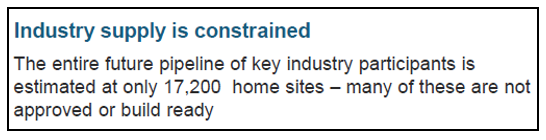

Ingenia points out that across the sector there are just 17,200 LLC sites identified and many have not got approvals yet.

Aura demonstrates medium rise a village advantage

Retirement villages have the advantage that they can go vertical, making land and zoning less of a challenge, and this new model is winning the new Baby Boomer customer.

Last week QLD’s Aura sent out a media release stating:

“Construction is now complete on the largest retirement living apartments on the Sunshine Coast, catering to today’s discerning Baby Boomer retirees who demand bigger and better accommodation.”

“Discreet age-appropriate design features allow our residents to age in place. Today’s retirees have no intention of ending up in nursing homes.”

Aura Holdings’ director Tim Russell says: “The Avenue Maroochydore (113 apartments) is addressing this gap in the Sunshine Coast market for high quality, spacious retirement living apartments near facilities and the water in a small, connected, supportive community.”

Aura Holdings’ director Tim Russell says: “The Avenue Maroochydore (113 apartments) is addressing this gap in the Sunshine Coast market for high quality, spacious retirement living apartments near facilities and the water in a small, connected, supportive community.”

“Our largest apartments are over 200sq m offering three bedrooms, two with ensuites, a third bathroom, a cook’s kitchen with dual ovens, Smeg appliances, a butler’s pantry, and a large balcony. The master bedroom’s walk-in robe is the size of regular double bedroom.”

“The heated magnesium pool will add to the community facilities in place including a gym, billiards room, library, wine room, courtyard entertainment areas and café.”

“There’s been a real shift amongst retirees towards apartment living in vertical living villages that require less land and can be built in enviable locations near vital facilities,” says Russell.

Apartments at The Avenue now sell from $465,000 to $1.35 million.

Aura purchased the 9,154sqm site in December 2016 for $6 million. It will be complete in 2021, making it a five-year project.

If the average sale price is $600,000, the project has an end value of $68 million (which they forecast in 2017 incidentally).

The winner in 2026 – villages or land lease?

Retirement villages should be growing faster than land lease in new builds in 2026, thanks to availability of land suitable for medium rise development and the offer of security, independence and control (translated: peace of mind and avoiding aged care).

But it will require an optimistic entrepreneurial spirit amongst village operators (such as Aura and Ryman). This is evident in spades in the land lease sector, combined with enthusiastic capital.

In summary, the winner will depend on the leadership of the individual operators in each sector. Who will you put your money on?