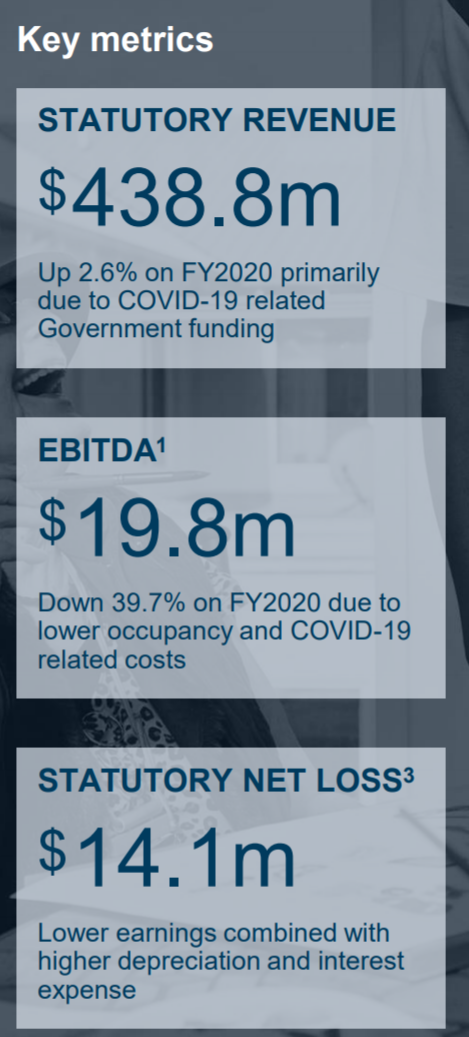

Another listed aged care operator that has experienced a turbulent year. While revenue increased 2.6% over the year, their EBITA dropped 40% to $19.8 million, resulting in a statutory net loss of $14.1 million.

Another listed aged care operator that has experienced a turbulent year. While revenue increased 2.6% over the year, their EBITA dropped 40% to $19.8 million, resulting in a statutory net loss of $14.1 million.

Over the 12 months the group had to contend with the negative brand impact of a large number of villages located in Victoria for COVID-19’s first wave, followed by COVID-19’s second wave, before it could fully recover.

On top of this, its board received the uninvited offer from Calvary followed by a second offer from Bolton Clarke. In the end, the board unanimously agreed to the Calvary offer, the equivalent of $2.20 per share (up from the original bid of $1.04), and is now in a Scheme of Arrangement to execute the deal.

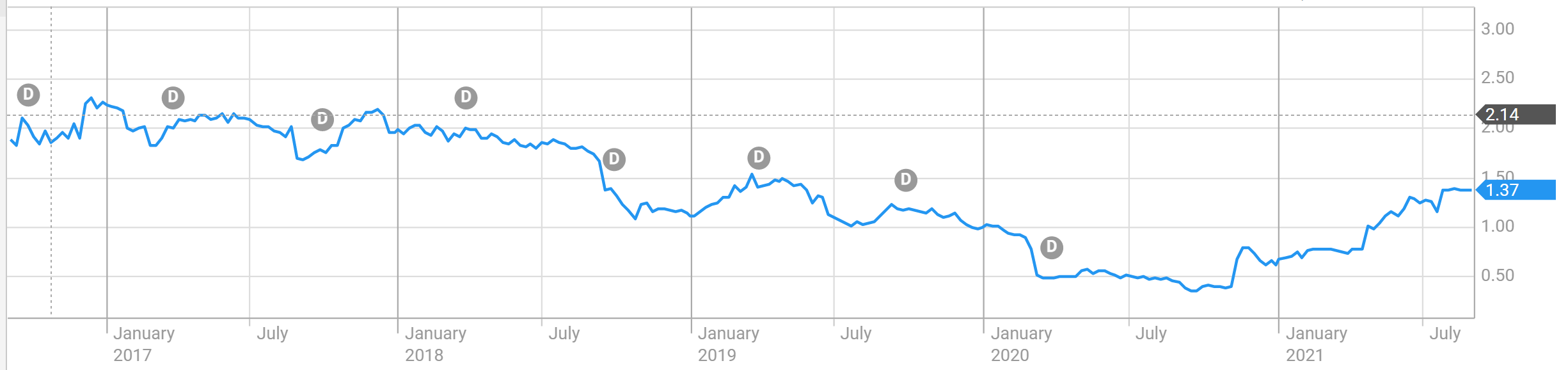

The company listed in 2014 at $2.57 a share.

It is interesting to see the additional cash Japara generated over the year by the sale of three of its homes.

It achieved the proceeds of $1.6 million by the closure and sale of its Wyong (NSW) home and $4.5 million (to be received in FY22) by the sale of its Chatswood (Sydney) home, Forest View.

It also sold and leased back for six years its Capel Sound (Victoria) home with net proceeds of $7.9 million.

The expected focus for Calvary on the completion of the acquisition will be to move occupancy back up to 92-94%, which will assist in driving the staff ratios back down to the industry standard of ~70%, allowing the company to regain profitability.