Home care operators are now just 51 business days away from a new program that will require them to toe the line between financial viability and the oversight of the regulator. It is time for blunt reality.

From 1 July 2025, home care providers will see their funding model shift from dependence on fixed management fees to a new activity-based model that will only deliver funding for services that are delivered – with new price caps looming in 12 months’ time. This requires a radical re-think of your finances and pricing.

The latest StewartBrown Aged Care Financial Performance survey has underlined the challenge facing operators.

Under Support at Home, the funding pool for care management funding has been capped at 10% of all quarterly client budgets.

Based in their December 2024 survey data, care management revenue currently makes up 18.7% of operators’ total revenue, while package management makes up 13%.

The shift to a 10% care management cap – and the removal of package management – means that operators must build this lost cash into their service pricing. It is not time for the timid or ‘we’ll see how it goes’.

Clear, decisive action is required and with the customer approval requirements, clear explanations and sell-in strategies will need to be in place – in just 51 business days' time.

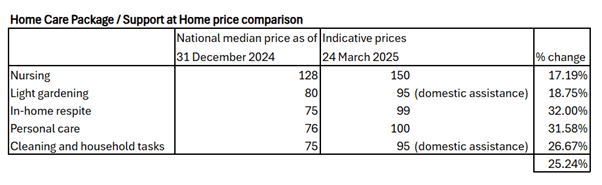

Indicative pricing not cutting it

The Department of Health and Aged Care released “indicative prices” for Support at Home – suggesting there will be at least an estimated 25% increase in service prices (pictured below) – but home care price caps are still due to be introduced from 1 July 2026 which will limit what operators can charge for services.

StewartBrown says the margin on service delivery (both internal and sub-contracted) will need to increase to 33% from the current 13% to maintain the present operating surplus – see below.

To deliver a 7.5% margin, operators need to be taking home $86.36 per client day.

To earn the 9.5% margin that StewartBrown says is required to ensure that operators are “investible”, the business needs to be putting $88.24 per client day in the bank.

How many operators are achieving these margins?

StewartBrown data shows the First 25% of programs they survey are just above this rate – $88.43 per client day.

But 20 to 30% of programs are operating at a loss. With 850 home care providers alone, this equates to 220 businesses losing cash that need to ask clients for more cash while also upgrading all their systems to deliver S@H. A big ask.

How can operators achieve or retain financially sustainable – and is ready to service the new Packages?

David Sinclair (pictured top) is a StewartBrown Partner and leads its advisory team on the transition to Support at Home.

He says the main concern for their clients – understandably – is setting appropriate service prices to compensate for the removal of package management and care management fees.

He advises providers to conduct a cost-up approach, determining service costs, necessary margins, and how these changes will affect their overall revenue, which he predicts will be increasingly shaky.

Some clients likely to lose services

He says pricing shifts will impact different types of clients, especially those maximising their Package funds. Will new 33% margins blow out Package dollars, for instance?

David said some clients may lose services due to price adjustments.

“Those clients that don’t utilise a lower Package will not be as impacted as those that use a large majority of their Package for services,” he underlined.

For example, if a care recipient is utilising 90% of their Package, a 30% increase in service prices will likely mean they max out their budget.

Providers therefore need strategies to minimise service reductions.

This could include tweaking their service pricing to balance cost recovery while maintaining client services.

Flat price increase? No.

Another strategy could involve differentiating prices for services based on the co-contribution rates (pictured below), for instance, lower prices for cleaning and higher prices for personal care.

David warns that flat price increases may not be the best approach – providers might need to make tailored price adjustments based on client needs.

Providers must also be cautious not to overprice, given the Government’s price caps are expected in 12 months ‘time.

Consent required for price increases

As discussed in our previous issue, operators also still need consent from their customers for any significant price changes – meaning all contracts, including those for existing customers, will need to be re-negotiated.

Law firm Maddocks says further guidance from the Aged Care Quality and Safety Commission (ACQSC) is still required for operators to fully understand the implications of any price increases.

“The regulator has been very strict on the principle that if you are increasing unit pricing, you must get their consent unless it’s an increase that is in line with your contract with the customer,” said its Partner and Healthcare Sector Leader Lucille Scomazzon.

“Most providers will have a CPI or slightly higher percentage in their contract in terms of the maximum amount that they can increase their prices by year, and it is still unclear how a provider will realign their fees with the Support at Home pricing framework.”

Then there is the red tape of definitions. Despite the Government’s promised ‘No Worse Off’ policy, the working definition seems to be that if clients receive the same level of service and don’t pay extra out-of-pocket, they are not considered ‘worse off’.

Lock down contractor prices for brokered services

Support at Home will also have a significant financial impact on operators’ contractor and brokerage arrangements.

Many providers previously took their revenue from package and care management fees rather than adding margins to contractor services.

With the new system, they must reconsider their contracts and ensure they build a sustainable revenue model.

David advises operators to consider locking in contractor prices to maintain financial viability.

As the registered provider, operators must also ensure contractor agreements include necessary oversight and compliance checks.

“If you subcontract and you have other organisation’s staff delivering services, you are still responsible for those services and staff and that flows from risk management to worker checks to the responsible duty for providers and management,” added Lucille.

Operators need to maximise billable hours

The other area for operators to consider is efficiency and productivity.

Government funding will likely allow for some degree of margin to be built into the Support at Home pricing, but they will also build in a baseline level of efficiency, meaning providers must optimise their operations if they want to maintain or grow their margins.

Workforce productivity, including minimising travel time and maximising billable hours, will be a key success factor.

The need to adopt technology to track finances and improve efficiency is also crucial.

Digital care management system The Lookout Way has upgraded its software to enable providers to track the profitability of individual visits and shifts, seeing exactly what their business earns daily.

“Having a system that can clearly show you what your costs are and what your income is from a shift from a visit from a client will be absolutely critical going forward,” said its co-founder and COO Nathan Betteridge.

Final advice for operators:

- Reevaluate your pricing structures to maintain revenue.

- Analyse the impact on clients to minimise service losses.

- Adjust your cost and revenue strategies to align with the new funding model.

- Review and renegotiate your contracts to ensure financial sustainability.

- Prepare for Government audits by maintaining accurate cost data and compliance records.

Opportunities for growth – and fairer funding

Despite the logistical challenges, Support at Home – and the 83,000 new Home Care Packages due in 2025-26 – offer significant growth opportunities for the sector, especially in clinical and allied health services, which have higher margins.

Contrary to sector concerns, David also expects that the new co-contribution scheme won’t deter care recipients from accessing services.

While full pensioners, who make up 90% of home care recipients, will pay a small co-contribution, for example, $5 per hour for personal care, this is still far less than what they would be charged for the same service in the private market.

Self-funded retirees, who are currently only 10% of Package recipients, may also see better value in the new system, as clinical care will be fully funded, potentially attracting them back into the system.

If operators can set their pricing appropriately, the benefits should flow beyond their own bottom line and ensure future price settings for the sector are fit for purpose.

“In my view, this is an opportunity for the sector to set a good benchmark for IHACPA and the Government as to what a sustainable price is for different services, and substantiate their pricing based on costs and a reasonable margin,” concluded David.

![]()