Australia’s only ASX listed pure retirement village operator is about to be privatised.

The announcement

Last Wednesday Aveo announced its Board of Directors had unanimously accepted the offer of $1.27 billion for the 100% purchase of the company by the Canadian investment fund Brookfield, which is the largest property group in the world. The agreed price is $2.195 per security. What they get is 96 communities with approximately 10,000 homes, 200 aged care beds and a pipeline of 5,000 village homesites and 670 aged care beds, for $1.29B.

The 131 page announcement released to the stock exchange outlined a timetable through to November with Aveo preparing documents to send to the security holders who hold 580,737,672 securities. It will be recommending they sell to Brookfield, and at the same time Aveo will not seek out alternative bids. The Brookfield offer is not conditional on finance or further due diligence.

Brookfield is offering security holders that they can either take the cash or transfer their investment into the Brookfield investment vehicle that will hold Aveo and join them in the new future for Aveo. (Brookfield calls this ‘stub equity’). Malaysia’s Mulpha who owns 24% of Aveo, and who has heavily influenced the company for the last 10 years, has not indicated whether it will stay in or sell. Its two directors on the Aveo board have recommended the ‘sale’ to Brookfield.

The deal should be done by Christmas, but the document allows it to extend to June next year.

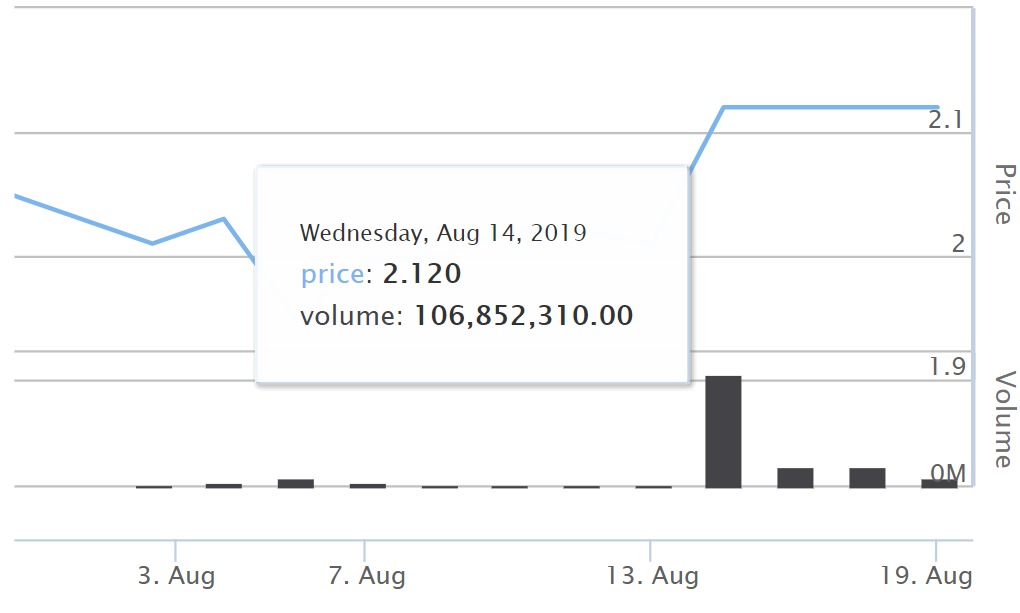

The immediate reaction

On the same day, last Wednesday 14th, a large number of security holders bailed out of Aveo at prices from $2.01 to $2.12. A total of 106,852,310 securities were sold and bought.

The sellers will still receive a four cents dividend announced in June, meaning they get $2.05 to $2.16 per security. They missed the $2.195 but they don’t have the risk that the deal won’t go ahead. Equally, the buyers should make a profit of 7.5 cents per security (after costs) which is 3.5% up to 18.5 cents or 20% in three months. The interesting thing is who was buying and what it delivers them. For instance, Morgan Stanley was an aggressive buyer ending up with 31.8 million shares and 5.48% of the company. UBS was a buyer and now has 6% and Mitsubishi financial group now has 7.57%.

We assume they want the short-term cash offer and not wishing to use the substantial holdings to ask for more.

The deal

The question that needs to be asked is; How was the price of $2.195 arrived at?

From the table above, from August last year, the Net Tangible Assets per security was assessed at $3.92.

The drop in value over 11 months is 44%. Does this mean that Brookfield is making the killing of the decade? That is unlikely, although no doubt it will be a very good deal – which we discuss further down.

Brookfield was the last buyer still at the table after multiple enquiries by interested purchasers, so the others ‘lifted the hood’ and then withdrew. Without being privy to the discussions it is reasonably easy to understand that the current uncertain regulatory world of retirement villages is a major problem. The declining housing market since July 2017 has taken 20% of village sales out of the market, just when Aveo was delivering a big pipeline of village homes (new developments like Newstead and at established villages like Durack).

Aveo, like many operators, also has a large percentage of its portfolio over 25 years old and in need of lots of capital.

And at the moment retirement villages are not ‘trusted’ by new consumers.

Brookfield will need to spend money, as we discuss below, but they are likely to have lots of cash coming their way: by our calculation Aveo has about 700 new village homes constructed and ready for sale (at $500,000 each say $350M) plus up to 700 established homes vacant and ready for sale – generating DMF income (at say 30% of $350,000 each say $74M).

Is the Brookfield purchase good for the sector? The answer is a resounding ‘yes’ in our view.

Aveo has great depth of experienced and quality management. More than any other village operator, Aveo has been pushing hardest across every sector of its business, gaining knowledge at every step.

(Pushing into assisted living with the Freedom portfolio strategy is one large-scale example – which some criticise but the US teaches us this is a big part of the future. The big commitment to quality food across its communities is less obvious but equally significant).

It is a great base for Brookfield to leverage.

The company, and the management, will now be released from responding to 3 monthly reporting to investors on the stock exchange. They can develop strategies that accept lower returns in the short-term to reinvest in their villages for higher returns and value in the medium-term.

The first actions will be investing in marketing and sales to generate cash from the existing vacant stock. As long as they are not fire sales, residents and families will benefit by receiving their cash earlier, new (fresh) residents will be entering the village, home values will rise and regulators will be appeased.

The second action will be capital investment in village rejuvenation to get them back to be ‘best in class’. This too will have an immediate benefit to residents - and sales.

Because ‘sales solve all problems’.

This will still be a lengthy process – say two years to get momentum. But in five years Brookfield may have invested, say, another $500 million but had revenue from vacant home sales of $400 million and a business value back up at say $3.50 per security. That would be an 84% return in five years.

Current and future residents would be enjoying the intangible and financial benefits. And regulators may be happier.

(But will small, private operators? The Brookfield balance sheet will allow it to have financial flexibility on things like ‘buybacks’ that small businesses will not be able to match. Nor will small businesses have the balance sheet to reinvest in older villages, meaning they will likely sell, and Brookfield could well be the only cashed up buyer that can absorb and then reinvest in the asset. Watch this space).

Further upside for Brookfield

Lendlease is taking its learnings from the Australian retirement village market to China. Last month they announced their first village of 900 homes, with plans to build four more next five years.

Aveo has experience in China. It had a 30% investment and provided the IP and management of the $326M ‘Tide and Health Campus’ one hour out of Shanghai.

Aveo will give Brookfield the expertise to expand into Asia and/or follow the New Zealanders into the UK and other markets.

Remember, Brookfield is the largest property group in the world and Aveo is now its retirement living base.

Will Mulpha and Geoff Grady stay the journey?

Mulpha has proven itself to be ‘patient capital’, it has backed the Aveo retirement model strategy for more than 10 years and Aveo CEO Geoff Grady has been journeying with Mulpha since around 2002, when Mulpha bought Sanctuary Cove out of receivership.

Grady was brought in to fix it, which he did. He took over as CEO of Aveo in 2013.

Grady says he wishes to continue in the retirement sector – and we assume leading Aveo. With his turnaround track record, intimate knowledge of the 1,400 homes to be sold and the pipeline of 5,000 to be developed and no retail investors to report to, he would look attractive.