Over half of residential aged care operators are forecast to still be making losses in FY2021-22 and FY2022-23 as COVID-19 subsidies wear off, according to StewartBrown’s latest 2020-2021 Aged Care Financial Performance Survey – and the discussion on a user pays system should be back on the cards.

The survey – which includes data from 269 providers (32% of the sector), 1,277 residential aged care homes (around 44% of homes) and 62,697 Home Care Packages (about 37% of Packages) – found 58% of residential care providers made an operating loss in FY21, up from 55% last year.

32% of homes made a cash loss, compared to 28% last year.

COVID-19 funding negates further losses

The average operating loss per provider was $2.1 million, a decrease on the $2.5 million loss the previous year.

Rural and remote providers were the worst off with 64% making a loss, but those in metro areas also fared poorly with 57% in deficit.

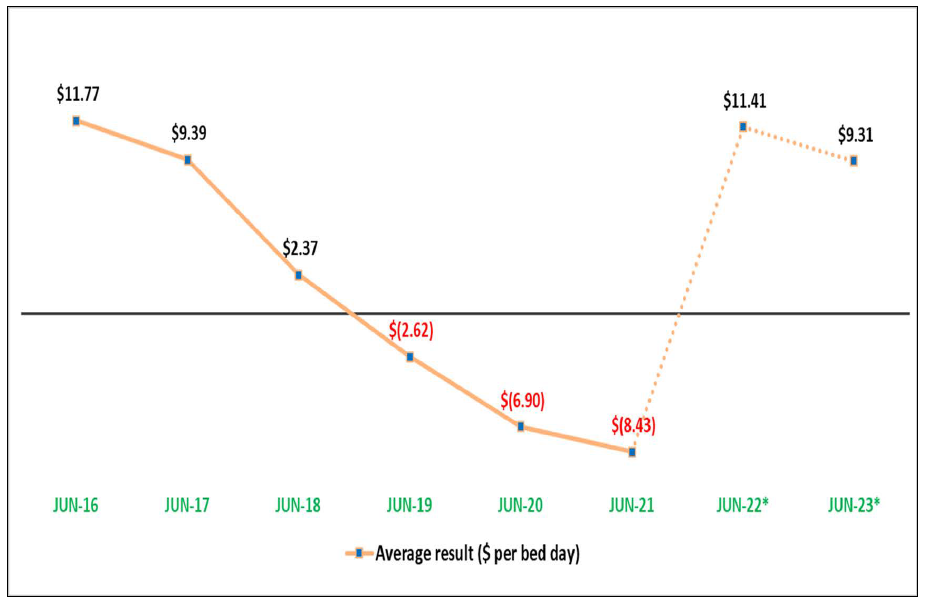

In total, aged care homes made an operating loss of $8.43 per bed per day in FY20-21, following a $6.90 loss in the previous year.

COVID-19 had a significant impact on this result, delivering a small surplus of $3.71 per bed per day for providers that didn’t have an outbreak.

Without this additional funding, the average loss would have been $12.14 per bed per day.

Top quartile still made profits

Some providers did manage to make a return despite the challenging conditions.

Operators in the top quartile had an average $1.8 million operating profit, compared to those in the bottom 25% which had an operating loss of $4.7 million.

Occupancy also continues to slide to 92% nationally, down from 93.6%, due to COVID-19, negative media around the Royal Commission and the increasing number of Home Care Packages.

Correspondingly, the median accommodation price as a percentage of the median house prices has also dropped to 73.4%, down from 80.6%.

Despite the losses, direct care minutes still increased to an average of 175.81 minutes, up 9.6% on June 2020.

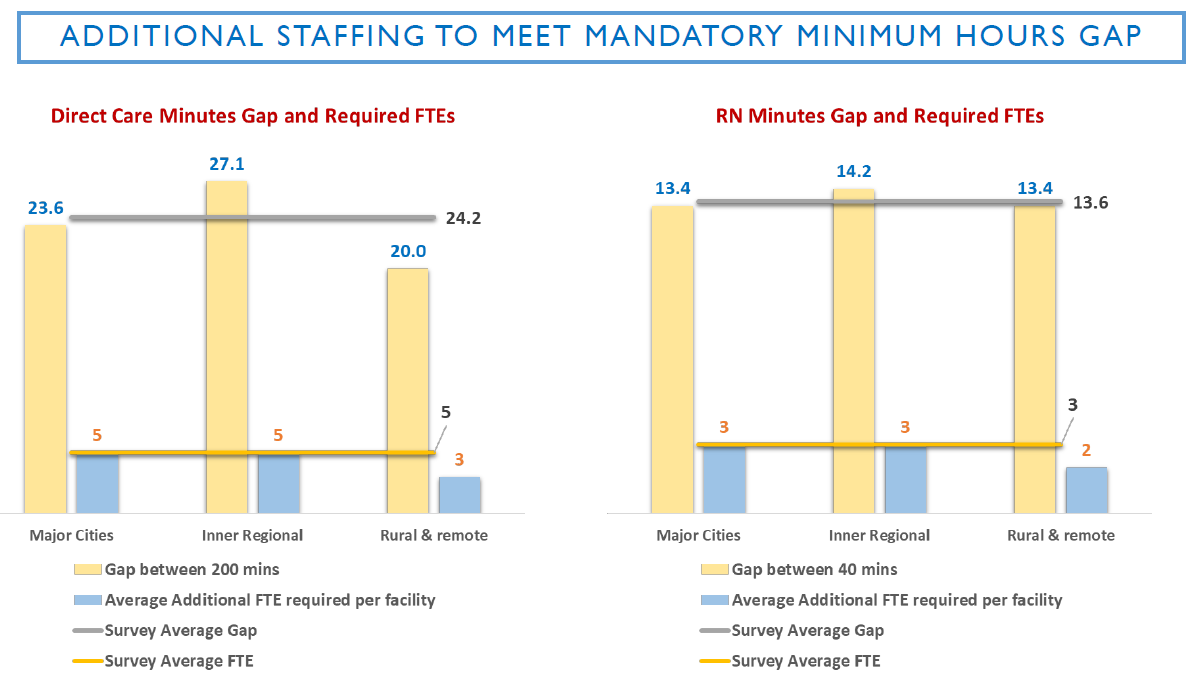

84% of providers falling short on new care minutes

But there is a large gap when it comes to the Government’s staffing reforms.

Only 16% of providers are currently meeting the 200 direct care minutes requirement being introduced from 1 July 2022 with just 11% meeting the future requirement for 40 minutes with an RN.

This will require an investment in additional staffing – cash that many operators don’t have.

This will require an investment in additional staffing – cash that many operators don’t have.

Speaking at StewartBrown’s 2021 Finance Forum last week, Senior Partner Grant Corderoy said the sector will continue to be financially challenged over the next two years, despite the $10 a day increase in the Basic Daily Care Fee.

“It’s not going to make a difference,” he said. “The loss of the COVID supplements is going to be really important – we think it should be retained.”

There will be a slight improvement because of the $10 a day supplement, with 53% of operators expected to be making an operating loss in 2022 – but this will then rise back up to 57% in 2023.

Consumers need to pay more – with new accommodation pricing

What is the solution then?

What is the solution then?

“We need to look at how to improve the funding and the consumer contribution,” said Grant.

Grant also recommended a look at accommodation pricing.

“It is inequitable for the consumer,” he said, noting that RADs deliver a much lower rate of rental than the DAP – but most consumers cannot afford a RAD and must therefore pay a DAP at a much higher accommodation ‘rental’.

His suggestion is a ‘deferred rental RAD’ – set at a lower price than the DAP to encourage people to take it up.

This would deliver operators an operating result of $11.41 per resident per day in June 2022 and $9.32 in June 2023.

This would deliver operators an operating result of $11.41 per resident per day in June 2022 and $9.32 in June 2023.

“This means that the co-contribution to care, part of the missing area is the accommodation cost,” said Grant.

“This has been lost in this current model. Providers aren’t increasing their accommodation prices, but I think that consumers who can afford it should pay a commensurate rate – a discounted rate if they are paying a RAD, but a commensurate rate like they are paying a DAP. This is a very important discussion that we have to have.”

We will delve into StewartBrown’s home care findings in next week’s Thursday SOURCE.