In a first for the retirement village sector, Retirement Living Council (RLC) representatives will meet with the Federal Aged Care Quality and Safety Commission (ACQSC) tomorrow (Thursday 6 March) to urgently counsel them on the impact of proposed Federal liquidity requirements on village operators that will potentially stunt the village business model.

The RLC is pushing for an extension of the 7 March response deadline on the legislation exposure draft. The sector was given just 15 working days to respond to the surprise liquidity imposts.

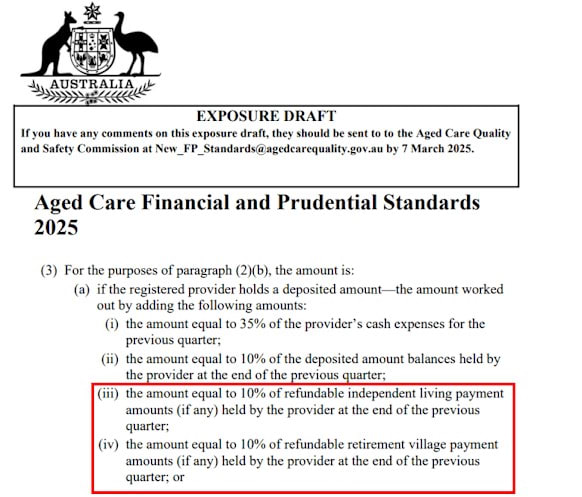

As we revealed last week, residential aged care providers that operate independent living units (ILUs) and retirement villages will have to retain 10% of ILU and retirement village refundable amounts as liquid funds under new aged care financial and prudential standards proposed by the ACQSC that are due to take effect from 1 July this year.

The RLC says this indicates the Commission does not understand the retirement village business model in that the average village resident occupies their home for eight to ten years (or say an average of 10% turnover a year). The operator makes 100% of their income from the DMF when they depart.

The Commission’s requirement of retaining 10% equates to one year’s full gross profit before overheads that would need to be siloed off.

Operators that would recycle capital into new developments or the next stage of the village would instead be forced to hold onto the cash to meet the Federal requirements, potentially stalling developments and undermining profits.

Reading the draft, the aged care services also do not need to be on the same physical site – meaning any operator with both residential aged care and retirement living would be captured under the legislation.

Requirements are a “half-baked thought bubble”: Daniel Gannon

The RLC brought together industry CFOs on Tuesday (4 March) to discuss the measures and The Weekly SOURCE understands that the peak body has now convened an emergency meeting with the ACQSC tomorrow (Thursday) to address the liquidity changes.

The regulator had maintained in last week’s Senate Estimates that it had consulted broadly when developing the liquidity ratios, including with the Older Persons Advocacy Network (OPAN), Council on the Ageing (COTA), Ageing Australia, McGrathNicol, StewartBrown, and the Aged Care Workforce Remote Accord – but the RLC or village operators were not mentioned.

RLC Executive Director, Daniel Gannon (pictured), did not mince his words in his analysis of the Government’s consultation with the village sector on the proposed changes.

“Meaning good and doing good are two very different things, which is something the Australian Government should be feeling this week,” he told The Weekly SOURCE.

“As reported yesterday, the Australian Government claims to have consulted with various stakeholders on liquidity ratios. If this is the case, then this group of stakeholders clearly does not understand the fundamentals of the retirement living sector – and maybe we shouldn't expect them to, given it’s not their core business.

“If this is not the case, and the government has in fact not consulted stakeholders – like it hasn’t consulted the RLC or retirement village operators – then this is a damning indictment on the way they’ve undertaken reform.

“This is starting to sound like a bad decision based on even worse advice – unintended consequences that impact operators and the residents they care for.

“Frustratingly, such ill-thought-out concepts can undermine innovation, progress, investor confidence, and future supply.

“While we supported the inclusion of retirement villages in the recent reforms to the Aged Care Act and applaud the Government for trialling our Shared Care framework, we had hoped it understood what our industry is, what it does, and how it is regulated.

“Retirement village operators acknowledge their increased role in delivering care services, but the requirements outlined in the proposed changes are a half-baked thought bubble.

“Serious policy reform deserves serious engagement and a serious consultation timeline. When consultation closes at the end of this week, we will have had just 15 working days to get our heads around this mess.

“Instead, we’re left with rushed reforms to meet a 1 July deadline, which is more about political expediency than lasting change.”

The Weekly SOURCE has also contacted Ageing Australia regarding the impact of the liquidity requirements on the retirement living sector but had yet to receive a response at the time of publication.

More news on this topic as it comes to hand.